Most drivers drop comprehensive and collision the day their SR-22 filing ends, but for financed vehicles, gap insurance requirements, and certain carrier discount structures, keeping full coverage through the entire filing period costs less than switching twice.

The Break-Even Point: When Keeping Full Coverage Beats Switching

Full coverage makes mathematical sense when your vehicle is financed, when your lender requires comprehensive and collision as a loan condition, or when your carrier's loyalty discount structure penalizes mid-term changes. Most non-standard carriers price coverage changes as policy rewrites rather than endorsements, which resets your anniversary date and eliminates accumulated discount tiers.

The math shifts at three thresholds. First, if your vehicle's actual cash value exceeds $8,000 and you carry a loan, the collision deductible ($500-$1,000 typical) is lower than your exposure if you total the vehicle while carrying liability-only. Second, if your post-reinstatement SR-22 insurance filing period is 3 years or longer, keeping continuous full coverage qualifies you for standard-market eligibility faster than toggling between liability-only and full coverage. Third, if your non-standard carrier offers a 15-20% discount for maintaining comprehensive and collision through the entire policy term, the discount pays for most of the collision premium by year two.

Run the numbers with your actual premium quotes. Compare the total cost of 36 months of full coverage against 36 months of liability-only plus the cost of adding collision when your filing period ends. Include the new-policy underwriting fee your carrier charges for mid-term changes, typically $50-$75. If the gap is less than $600 over three years, the stability of continuous full coverage outweighs the marginal savings of liability-only.

Lender Requirements During SR-22 Filing

Auto lenders require comprehensive and collision coverage as a loan condition regardless of your SR-22 filing status. The loan contract specifies minimum coverage limits and maximum deductibles, typically $500 or $1,000. If you drop to liability-only during your filing period, the lender will force-place coverage at rates 200-300% higher than voluntary market premiums and add the cost to your loan balance.

Force-placed coverage protects the lender's interest, not yours. It covers the loan payoff amount but does not cover your deductible, does not provide gap coverage if you owe more than the vehicle's value, and does not include liability protection. If you total the vehicle while carrying force-placed insurance, you remain liable for the gap between the settlement and your loan balance.

Pay the voluntary full coverage premium during your SR-22 period. The premium will be higher than pre-suspension rates, but it will be 40-60% lower than force-placed coverage and will include liability protection your lender's policy does not provide. Most non-standard auto insurance carriers offer payment plans that split the premium into monthly installments, reducing the immediate cash outlay.

Compare car insurance rates in your state

Get quotes from licensed carriers — no obligation, no spam, results in minutes.

Get Your Free Quote✓ No Obligation Required✓ Licensed Carriers Only✓ Available Nationwide✓ Free to Compare

Gap Insurance and Total Loss Scenarios

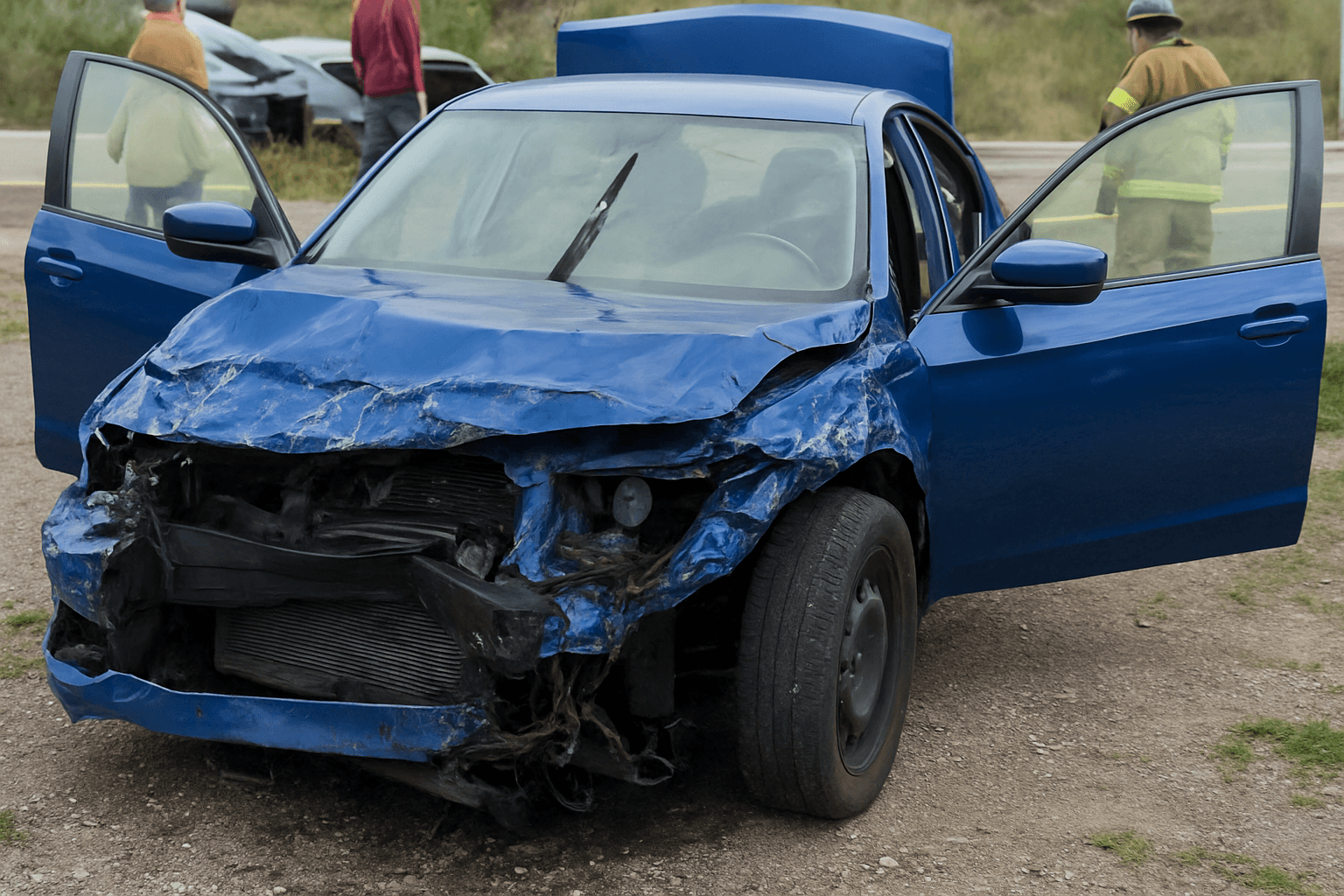

Gap insurance pays the difference between your vehicle's actual cash value and your remaining loan balance if the vehicle is totaled. Most drivers finance vehicles at 110-130% loan-to-value ratios, meaning they owe more than the vehicle is worth for the first 24-36 months of the loan. If you total a financed vehicle during your SR-22 filing period while carrying liability-only coverage, you remain liable for the full loan balance with no vehicle.

Carriers sell gap insurance as an endorsement to full coverage policies, not as standalone coverage. The cost is typically $40-$80 per year when added at policy inception. If you drop comprehensive and collision during your filing period, you lose gap coverage even if you paid for it upfront, and most carriers will not reinstate it without underwriting the vehicle as a new policy.

The claim scenario drives the decision. If you finance a $15,000 vehicle with a $2,000 down payment and total it 18 months into a 60-month loan, your loan balance will be approximately $11,000 while the vehicle's actual cash value will be $9,000-$10,000. Without gap insurance, you owe the lender $1,000-$2,000 after the collision settlement, plus you need a replacement vehicle. Gap insurance eliminates that liability for $120-$240 over three years.

Carrier Discount Structures and Policy Continuity

Non-standard carriers reward policy continuity with tiered discounts that accumulate over 12-36 months. The structure varies by carrier, but the pattern is consistent: 5% after 12 months of continuous coverage, 10% after 24 months, 15% after 36 months. These discounts apply to the total premium, not just the liability portion, so they compound fastest when you maintain comprehensive and collision through the entire filing period.

Mid-term coverage changes reset the discount clock. If you drop comprehensive and collision 18 months into a 36-month SR-22 filing period, then add it back 12 months later, you lose 18 months of discount accumulation. The carrier treats the coverage addition as a policy rewrite, which restarts your anniversary date and eliminates your 10% continuity discount. Over the remaining 6 months of your filing period, you forfeit approximately $150-$300 in discount value.

The math favors stability. A driver paying $180/month for full coverage with a non-standard carrier receives a $18/month discount after 12 months ($216 annual savings), $36/month after 24 months ($432 annual savings), and $54/month after 36 months ($648 annual savings). If that driver drops to liability-only coverage at $110/month to save $70/month, but loses the continuity discount when they add collision back, the net savings over 36 months is $1,680 in avoided premiums minus $1,296 in forfeited discounts, yielding $384 total savings over three years—$10.67 per month.

When Liability-Only Coverage Makes Sense Instead

Liability-only coverage is the correct choice when your vehicle is paid off, when its actual cash value is below $5,000, or when your collision deductible exceeds 50% of the vehicle's value. A vehicle worth $4,000 with a $1,000 collision deductible leaves you with a maximum $3,000 payout if you total it, and the three-year cost of collision coverage will exceed that amount for most SR-22 filers.

The threshold calculation is straightforward. Multiply your monthly collision premium by the number of months remaining in your SR-22 filing period, then subtract your deductible from your vehicle's actual cash value. If the total collision cost exceeds the net claim payout, drop the coverage. For example, a driver with 24 months remaining in their filing period paying $45/month for collision on a vehicle worth $4,500 will pay $1,080 in premiums for a maximum $3,500 net payout ($4,500 value minus $1,000 deductible). The break-even threshold is $3,500 in vehicle value; below that, liability-only wins.

Consider non-owner SR-22 coverage if you sold or totaled your vehicle during the suspension period and do not plan to purchase a replacement until after your filing period ends. Non-owner policies satisfy your state's SR-22 filing requirement without insuring a specific vehicle, and the premium is typically 40-50% lower than full coverage on an owned vehicle. You cannot drive a vehicle you own while carrying a non-owner policy, but if you rely on rideshare, public transit, or borrowed vehicles, non-owner coverage meets the legal requirement at the lowest cost.

State-Specific Filing Period Length and Coverage Strategy

SR-22 filing periods range from 1 year to 5 years depending on your state and the violation that triggered the requirement. DUI convictions typically require 3-year filings in most states, with California, Florida, and Ohio requiring 3 years, Texas requiring 2 years, and Illinois requiring 3 years for first offenses. Points-related suspensions and uninsured-driving violations typically require 1-3 years, while repeat DUI offenses trigger 5-year filing periods in several states.

The filing period length changes the full-coverage calculation. A 1-year filing period makes toggling coverage viable because you reach standard-market eligibility quickly and the discount forfeiture window is short. A 5-year filing period makes continuous full coverage more valuable because the discount accumulation compounds over a longer term and because standard carriers weigh policy stability more heavily when you apply for coverage after the filing period ends.

Verify your state's filing period with your carrier or DMV before choosing coverage limits. Some states count the filing period from the conviction date, others from the license reinstatement date, and a few count from the date the SR-22 form is filed. The difference can shift your filing end date by 6-12 months, which changes the break-even calculation for continuous full coverage versus liability-only.