Updated May 2026

What Is Property Damage Liability Insurance?

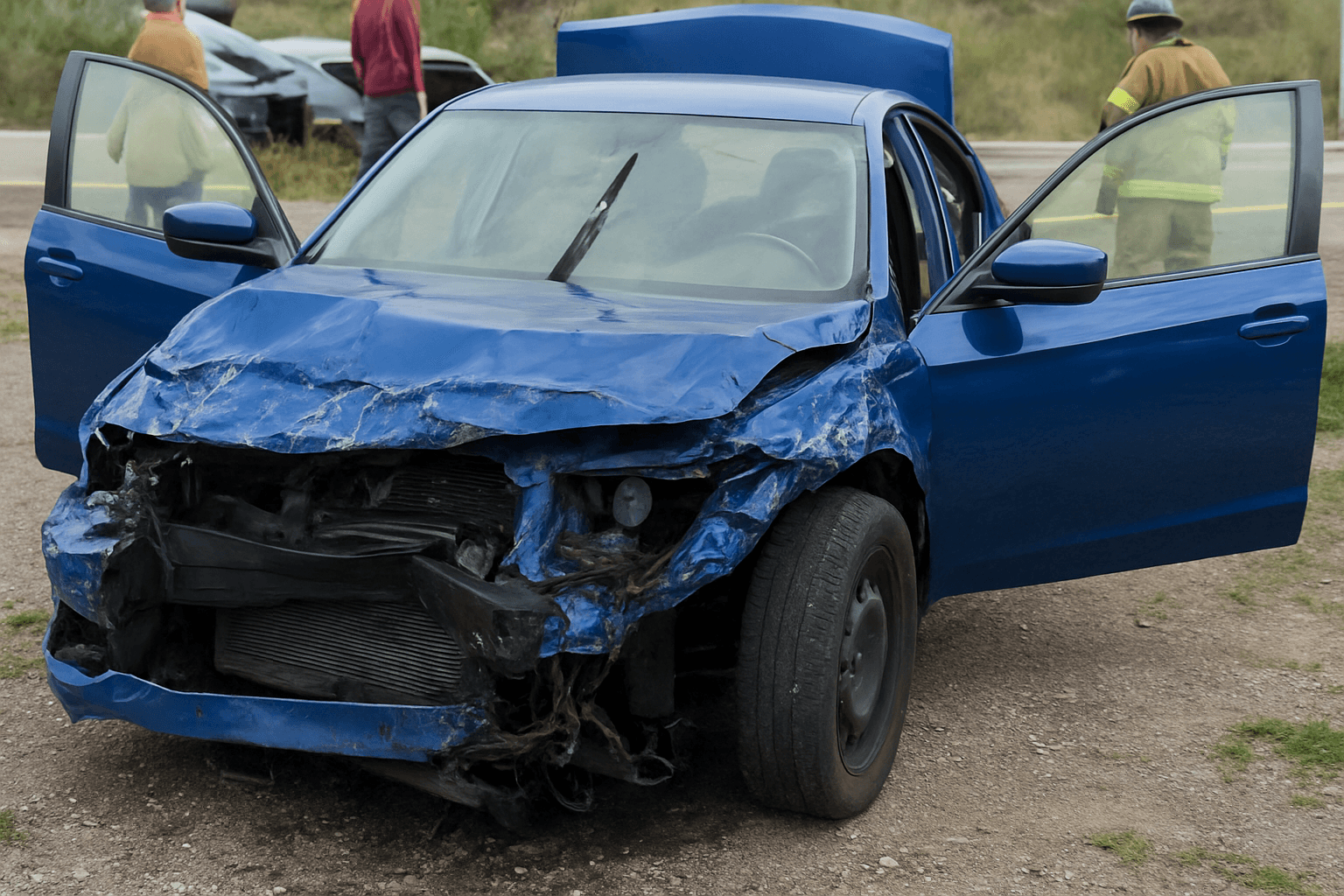

Property Damage Liability (PD) covers the cost of damage you cause to another person's property in an at-fault accident. That includes their vehicle, but also structures like guardrails, fences, buildings, or utility poles. Your insurer pays the other party's repair bills up to your policy limit. If damage exceeds your limit, you're personally responsible for the difference.

- You rear-end a car at a stoplight. The other driver's vehicle sustains $8,200 in damage. You carry $10,000 in property damage liability. Your insurer cuts a check for $8,200 to the other driver's repair shop. You pay nothing out of pocket. Your own car's damage isn't covered under this policy—you'd need collision for that.

- You lose control on ice and slide into two parked cars. Combined damage totals $34,000. Your policy limit is $25,000. Your insurer pays the first $25,000. You're personally liable for the remaining $9,000, which the other parties can pursue through a lawsuit or payment agreement. After reinstatement, many drivers carry state minimums to reduce premium—but this is the gap that creates.

- You swerve off the road and take out a neighbor's wooden fence and brick mailbox. Repairs cost $3,400. Your $10,000 property damage liability limit covers the claim in full. This is the coverage that pays for non-vehicle property damage—structures, landscaping, or anything else you hit.

How Much Does Property Damage Liability Insurance Cost?

Property Damage Liability typically adds $15–$35 per month to your premium, or approximately $180–$420 annually, depending on your state and coverage limit.

- Coverage limit selected—$25,000 limits cost less than $100,000 limits, but higher limits protect you from personal liability in serious accidents.

- Your driving record—recent at-fault accidents or violations increase PD liability premiums because you're statistically more likely to cause property damage again.

- State minimum requirements—states with higher mandatory minimums often have higher base premiums for this coverage.

- ZIP code and local repair costs—areas with expensive vehicle repair shops or high collision rates see higher property damage liability premiums.

- Vehicle type—if you drive a heavy truck or SUV, insurers may charge more because those vehicles tend to cause more damage in collisions.

See How Much You Could Save

Get personalized property damage liability insurance quotes in minutes.

Who Needs Property Damage Liability Insurance?

Anyone driving a vehicle needs Property Damage Liability—it's legally required in every state. After license reinstatement, you need it to satisfy SR-22 filing requirements. If you own assets like a home, savings account, or retirement fund, carry limits well above your state's minimum—$50,000 or $100,000—to protect those assets from lawsuits after an at-fault accident.

Carry your state's minimum if premium is the only priority and you have no assets to protect. Carry $50,000 or higher if you own a home, have savings, or want protection against personal liability. The difference in premium between a $10,000 limit and a $50,000 limit is typically $8–$15 per month—a small cost compared to the financial exposure of being underinsured.